×

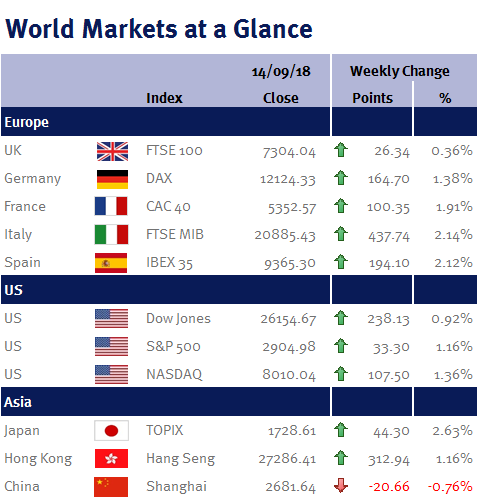

Week ending 14th September 2018.

17th September 2018

There was a distinct lack of exuberance shown by equity markets this week to news that Steven Mnuchin, the US Treasury Secretary, had offered to restart talks with China in order to de-escalate the trade spat.

While this was disappointing, it was understandable given last week’s US employment data, coupled with the fact that it is Donald Trump and not Steve Mnuchin in the driving seat – and of course, he could easily decide to impose further tariffs on China in advance of any talks (and use their removal as a carrot).

Interestingly, while last week’s US employment data showed wage growth had picked up (giving a green light to the Fed to keep progressing on its higher interest rate path), this week’s US core CPI fell to 2.2% from 2.4%. Furthermore US PPI showed its first month-on-month decline in eighteen months. This suggests to me that inflationary pressures are far from rampant in the US and, as I have previously said in these weekly summaries, I would not be surprised if the Fed’s conviction in the need for higher interest rates starts to decline.

As expected the BoE left interest rates unchanged this week, while the accompanying minutes had a slightly dovish tone due to comments on Brexit uncertainty. Consequently, I was therefore gobsmacked to read that the BoE Governor, Mark Carney, told cabinet ministers yesterday (Thursday 13 September 2018) that a no-deal Brexit would probably see UK interest rates rise!

In Europe, the ECB also left interest rates unchanged and reiterated its commitment to keeping rates unchanged “at least through the summer of 2019”. The ECB also lowered its growth forecasts for this year and next (to 2% and 1.8% from 2.1% and 1.9% respectively). CPI inflation forecasts stayed the same at 1.7% for 2018, 2019 and 2020.

This coming week we have UK CPI and UK retail sales data; eurozone CPI and PMI; and US housing data (housing starts; building permits and home sales).

Ian Copelin, Investment Management Expert*

*Ian Copelin is an Investment Director at Wealth at Work Limited which is a member of the Wealth at Work group of companies

The latest market updates are brought to you by Investment Managers & Analysts at Wealth at Work Limited which is a member of the Wealth at Work group of companies.

Links to websites external to those of Wealth at Work Limited (also referred to here as 'we', 'us', 'our' 'ours') will usually contain some content that is not written by us and over which we have no authority and which we do not endorse. Any hyperlinks or references to third party websites are provided for your convenience only. Therefore please be aware that we do not accept responsibility for the content of any third party site(s) except content that is specifically attributed to us or our employees and where we are the authors of such content. Further, we accept no responsibility for any malicious codes (or their consequences) of external sites. Nor do we endorse any organisation or publication to which we link and make no representations about them.