×

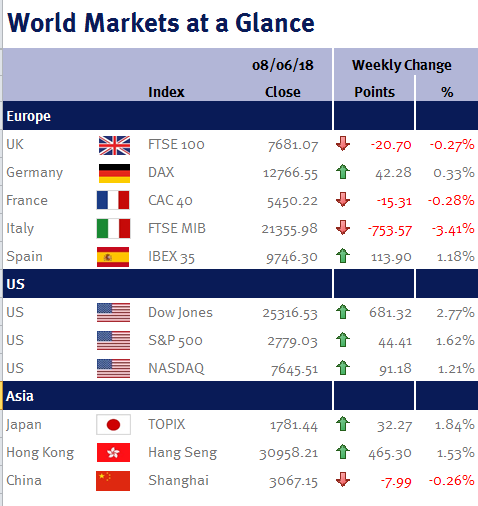

Week ending 8th June 2018.

11th June 2018

It is good to see that markets are finally starting to ignore the majority of Donald Trump’s tweets and off-the-cuff comments, appreciating that this is simply part of his negotiating tactics in the ‘new world’ of social media and 24-hour news.

As such, equity markets brushed aside trade-war fears and instead focused on the continuation of the upbeat economic data following last Friday’s (1 June 2018) US employment report.

For example, in the UK, PMI data for both construction and services nicely beat economist estimates, while both the BRC and Barclaycard reported that consumer spending grew strongly (although two warm bank holiday weekends, coupled with the Royal Wedding, clearly helped as sales of summer clothes and BBQs jumped).

However attention may well turn back to trade as G7 leaders meet in Quebec today (Friday 8 June 2018) and tomorrow, with the EU and Canada threatening retaliatory measures unless Donald Trump reverses his planned tariffs on steel and aluminium imports.

We also have a busy and eventful week ahead. While the summit between Donald Trump and Kim Jong Un will undoubtedly take centre stage in the media, the world’s three most powerful central banks hold monetary policy meetings.

While I expect no change from the ECB meeting, again the accompanying statement will be the main focus after the ECB’s chief economist, Peter Praet, acknowledged this week that the ECB’s meeting will be key for reaching a decision on when to end the ECB’s QE program, given that eurozone inflation is starting to converge with their target (an inflation rate below, but close to, 2% over the medium term).

As I highlighted last week (please see here), while eurozone inflation jumped to 1.9% from 1.2% in April, this was clearly impacted by the higher oil price as the core inflation rate (which excludes volatile items such as food and energy and is seen as a signal of where headline inflation will head) came in at just 1.1%. Additionally, similar to the UK, eurozone Q1 economic data was soft. Consequently, I would speculate that the ECB policymakers may actually want to wait a little longer for evidence that inflation is actually increasing and that the underlying strength in the eurozone economy is strengthening.

In Japan, the BoJ is very unlikely to change course given the continuation of low inflation.

We also have US CPI, PPI, retail sales, industrial production and the University of Michigan Consumer Sentiment index; eurozone CPI, industrial production and employment; UK employment data (unemployment rate, weekly earnings) along with CPI, PPI, retail sales and industrial production; and Chinese CPI, PPI, retail sales and industrial production.

Additionally, the Brexit bill goes to a vote in Parliament.

Ian Copelin, Investment Management Expert*

*Ian Copelin is an Investment Director at Wealth at Work Limited which is a member of the Wealth at Work group of companies

The latest market updates are brought to you by Investment Managers & Analysts at Wealth at Work Limited which is a member of the Wealth at Work group of companies.

Links to websites external to those of Wealth at Work Limited (also referred to here as 'we', 'us', 'our' 'ours') will usually contain some content that is not written by us and over which we have no authority and which we do not endorse. Any hyperlinks or references to third party websites are provided for your convenience only. Therefore please be aware that we do not accept responsibility for the content of any third party site(s) except content that is specifically attributed to us or our employees and where we are the authors of such content. Further, we accept no responsibility for any malicious codes (or their consequences) of external sites. Nor do we endorse any organisation or publication to which we link and make no representations about them.