×

Week ending 23rd February 2018.

26th February 2018

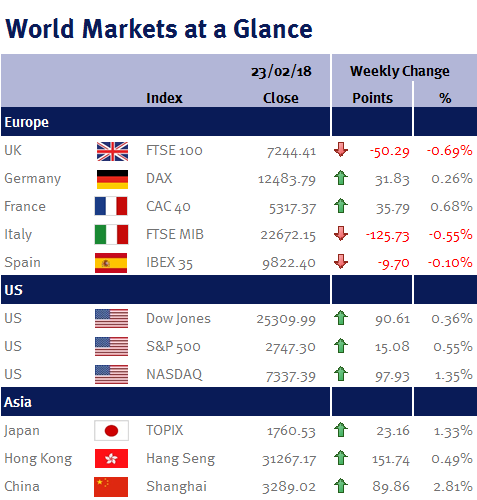

There was further insight into the thoughts of the UK and US Central Banks this week; however, the direction of equity markets was largely influenced by many companies announcing their 2017 earnings.

The minutes of the January FOMC meeting released on Wednesday paved the way for Jerome Powell’s first FOMC meeting as Federal Reserve Chair to result in raising the US interest rates. Minutes showed that Federal Reserve members are becoming more confident in their economic outlook, which coupled with expectations of continuing strength in the labour market, leads them to be optimistic about hitting their inflation target.

In the UK this week, Mark Carney, Governor of the Bank of England gave testimony on the inflation report and whilst he is unable to commit to a likely path of future interest rates, his choice of words does help to influence investor expectations. Ultimately, future economic data will determine interest rates and the act of raising interest rates will impact future data; so investors and central bankers need to remain vigilant and respond to data as and when it is released. Unemployment data this week didn’t help the case for raising UK rates, as it unexpectedly rose for the first time in nearly two years, rising from 4.3% to 4.4% between October and December. Average weekly earnings on the other hand, came in 0.1% above expectations at 2.5% and whilst still lagging the rate of inflation (CPI 3.0%), the gap is narrowing. Productivity in the UK was also reported this week to have been the best since the 08/09 recession.

Next week, 2017 corporate earnings releases continue, the new Fed Chairman, Jerome Powell, will deliver his first semi-annual testimony on the US economy and monetary policy on Tuesday and Theresa May will give a speech outlining her Brexit strategy on Friday.

Peter Quayle, Investment Management Expert*

*Peter Quayle is a Fund Manager at Wealth at Work Limited which is a member of the Wealth at Work group of companies

The latest market updates are brought to you by Investment Managers & Analysts at Wealth at Work Limited which is a member of the Wealth at Work group of companies.

Links to websites external to those of Wealth at Work Limited (also referred to here as 'we', 'us', 'our' 'ours') will usually contain some content that is not written by us and over which we have no authority and which we do not endorse. Any hyperlinks or references to third party websites are provided for your convenience only. Therefore please be aware that we do not accept responsibility for the content of any third party site(s) except content that is specifically attributed to us or our employees and where we are the authors of such content. Further, we accept no responsibility for any malicious codes (or their consequences) of external sites. Nor do we endorse any organisation or publication to which we link and make no representations about them.