×

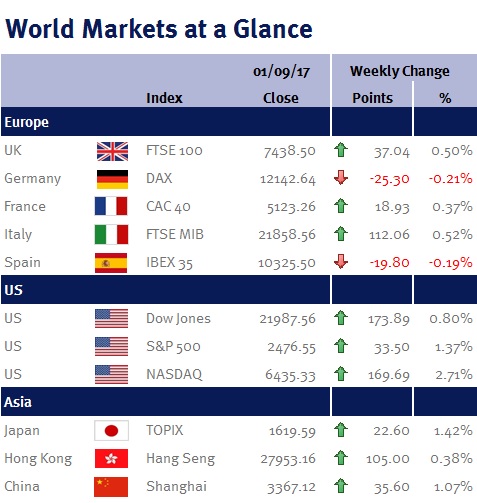

Week ending 1st September 2017.

4th September 2017

On Tuesday (29 August 2017) we had the typical knee-jerk panic reaction that you would expect after North Korea fired a missile over Japan (equity markets were rattled, while safe haven assets gained).

However, these moves were very quickly reversed after positive economic data boosted confidence that the non-inflationary global growth is ticking along nicely (the goldilocks scenario).

In the US, annualised Q2 GDP growth figures were revised up from 2.7% to 3% – the fastest pace in two years helped by stronger household spending and a bigger gain in business investment; while the core PCE, the Fed’s preferred inflation gauge, remained well below their 2% target at 1.4% in July on an annualised basis.

Additionally, while US non-farm payroll data was robust, the 156,000 increase was slightly below estimates. This coupled with the above PCE inflation and a small increase in the unemployment rate to 4.4% (from 4.3%), supports my view that the Fed will have difficulty justifying another interest rate increase this year – and that’s even before the potential fallout from Hurricane Harvey (which will have an impact on most economic indicators and data over the coming months and quarters).

As a result, I continue to believe that it is unlikely that the ECB will feel comfortable tapering its QE program just yet, especially given the recent strength of the euro (which is likely to further lower inflation expectations). And we could find out next week what policymakers are thinking as we have a press conference following the ECB’s monetary policy meeting (Thursday 7 September 2017).

Also next week we have eurozone PMI and the US Beige Book.

Ian Copelin, Investment Management Expert*

*Ian Copelin is an Investment Director at Wealth at Work Limited which is a member of the Wealth at Work group of companies

The latest market updates are brought to you by Investment Managers & Analysts at Wealth at Work Limited which is a member of the Wealth at Work group of companies.

Links to websites external to those of Wealth at Work Limited (also referred to here as 'we', 'us', 'our' 'ours') will usually contain some content that is not written by us and over which we have no authority and which we do not endorse. Any hyperlinks or references to third party websites are provided for your convenience only. Therefore please be aware that we do not accept responsibility for the content of any third party site(s) except content that is specifically attributed to us or our employees and where we are the authors of such content. Further, we accept no responsibility for any malicious codes (or their consequences) of external sites. Nor do we endorse any organisation or publication to which we link and make no representations about them.