×

Week ending 2nd June 2017.

5th June 2017

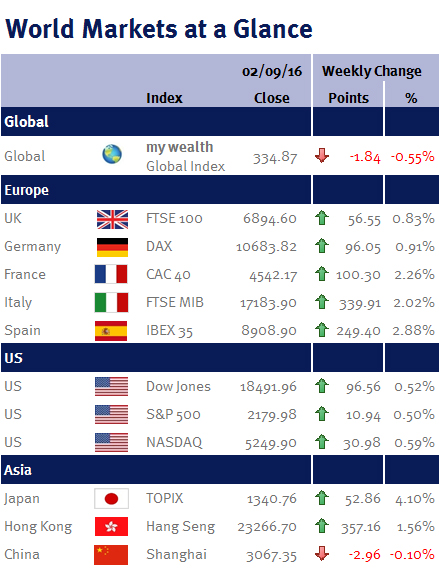

Global stocks traded higher, with all three of the major US indices making new all-time highs, following comments from Federal Reserve policymakers on the path of US interest rates and Mario Draghi’s dovish message to the European Parliament.

At his appearance at the European Parliament’s Economy Committee in Brussels, Mario Draghi, the ECB President, reiterated his view that massive stimulus is still required. While he acknowledged that Europe’s economy was improving, he said that it still needed expansive monetary stimulus to restore inflation as “domestic cost pressures, notably from wages, are still insufficient to support a durable and self-sustaining convergence of inflation toward our medium-term objective”.

Giving support to his view, Eurostat on Wednesday (31 May 2017), said that eurozone CPI decelerated from 1.9% in April to 1.4% in May (the weakest reading this year), while the core measure (which excludes volatile items such as food and oil) slowed to 0.9% from 1.2%.

And as for the US Fed policymakers, Jerome Powell, Robert Kaplan (the Fed’s Dallas President) and John Williams (the Fed’s San Francisco President – although he doesn’t currently have a vote on monetary policy), all reaffirmed that a total of three interest-rate increases makes sense for the world’s biggest economy this year.

I would though sound a note of caution on how fast the central bank can keep tightening: US inflation has started to slip away from the Fed’s target and May’s US employment data disappointed.

The Fed’s preferred inflation measure, the PCE, fell from 1.9% in March to 1.7% in April, while the core measure slowed to 1.5% – its weakest annual pace since December 2015), while the nonfarm payrolls showed 135,000 jobs were added to the US economy versus expectations of 178,000.

While the shortfall is unlikely to dissuade Fed policymakers from increasing US interest rates at their next meeting on 13-14 June 2017, I believe that it could make it more difficult for them to follow through with a third increase later in the year, as they continue to indicate (please see above).

This week coming we will find out if the political polls have been correct in the UK election after failing to predict the Conservative majority in 2015 or the ‘Leave’ vote in last June’s EU Referendum.

When Theresa May called the general election, ahead of what is expected to be a tough set of Brexit negotiations, the Conservatives had a 20+ point lead in the polls, suggesting that she could easily outdo Margaret Thatcher’s 144 seat majority in 1983. However, mathematically getting such a large majority today maybe difficult given the support for the SNP (56 seats at the last election versus just 2 seats in 1983); Plaid Cymru (3 versus 2); DUP (8 versus 3); and Sinn Féin (4 versus 1). Furthermore, since the election was called Theresa May’s seemingly unassailable lead has narrowed significantly, with polling company YouGov this week projecting a hung parliament.

Given that the pound and UK equity market rallied after Theresa May called the snap election (as a large Conservative majority should, theoretically, make it easier for the Tories to agree a transitional arrangement and prolong access to the single market beyond March 2019), anything less than an increased majority (to say 35-50 seats) for Theresa May could disappoint the UK financial market as this is probably the minimum required as a more realistic ‘workable’ majority.

Ian Copelin, Investment Management Expert*

*Ian Copelin is an Investment Director at Wealth at Work Limited which is a member of the Wealth at Work group of companies

The latest market updates are brought to you by Investment Managers & Analysts at Wealth at Work Limited which is a member of the Wealth at Work group of companies.

Links to websites external to those of Wealth at Work Limited (also referred to here as 'we', 'us', 'our' 'ours') will usually contain some content that is not written by us and over which we have no authority and which we do not endorse. Any hyperlinks or references to third party websites are provided for your convenience only. Therefore please be aware that we do not accept responsibility for the content of any third party site(s) except content that is specifically attributed to us or our employees and where we are the authors of such content. Further, we accept no responsibility for any malicious codes (or their consequences) of external sites. Nor do we endorse any organisation or publication to which we link and make no representations about them.