×

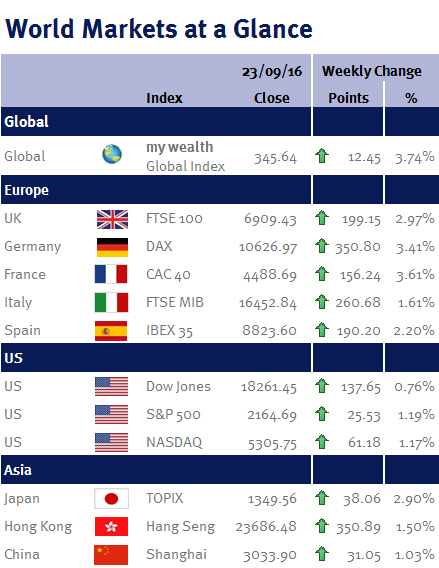

Week ending 21st October 2016.

24th October 2016

As there was little economic data out of the US to give the market any further clues on the exact timing of the Federal Reserve’s interest rate increase, all eyes were on the European Central Bank (ECB), where the governing council met to discuss monetary policy.

However it wasn’t the ECB’s interest rates decision (which was, as expected, unchanged at -0.4%) that was of interest: it was the subsequent press conference with the ECB President, Mario Draghi.

Although Mario Draghi said that no decision had been made on whether or not to extend its quantitative easing (QE) program beyond March 2017, he signalled that it wouldn’t come to an “abrupt” end – which helped send European bourses higher.

In the UK, headline CPI inflation accelerated to 1% in September, having been 0.6% in August. The largest contributions to the upward move came from clothing and footwear (+5.2% during the month – reversing recent heavy discounting and weather distortions), while transport (predominately fuel) advanced 1.2%.

Whilst it was a big jump, the Office of National Statistics stated that inflation has yet to fully reflect the recent weakness in sterling (while a weaker pound helps exporters, it makes our imports more expensive) – and we know from the recent spat between Tesco and Unilever (‘Marmite-gate’) that we can expect more price rises to come through.

Furthermore, if the sharp decline in the oil price seen in the fourth-quarter of 2015 (when it fell from just over $50 per barrel to just below $27) doesn’t repeat itself, fuel is likely to make a large upward contribution to the CPI over the next 12 months (oil is currently $49.96 per barrel).

Elsewhere the Chinese economy appears to have stabilised after the turbulence seen in 2015. Third-quarter GDP grew at an annual rate of 6.7%, unchanged from the previous two quarters. However, China’s six months of rising exports came to an end, dropping 10% in September – suggesting that global demand remains lacklustre.

Ian Copelin, Investment Management Expert*

*Ian Copelin is an Investment Director at Wealth at Work Limited which is a member of the Wealth at Work group of companies

The latest market updates are brought to you by Investment Managers & Analysts at Wealth at Work Limited which is a member of the Wealth at Work group of companies.

Links to websites external to those of Wealth at Work Limited (also referred to here as 'we', 'us', 'our' 'ours') will usually contain some content that is not written by us and over which we have no authority and which we do not endorse. Any hyperlinks or references to third party websites are provided for your convenience only. Therefore please be aware that we do not accept responsibility for the content of any third party site(s) except content that is specifically attributed to us or our employees and where we are the authors of such content. Further, we accept no responsibility for any malicious codes (or their consequences) of external sites. Nor do we endorse any organisation or publication to which we link and make no representations about them.